Contracting through a Pty Ltd company in Australia involves a genuinely different set of rules from anything in the UK or elsewhere — there’s no direct equivalent of IR35, but there is something that rhymes with it, and it interacts with a uniquely Australian mechanism (dividend imputation) that has no counterpart at all in most other tax systems.

The first question: is this a genuine business, or attributed income?

Before anything else, a contractor operating through a company needs to work out whether their income is a genuine Personal Services Business (PSB) or whether Personal Services Income (PSI) attribution rules apply. This determination, governed by ATO ruling TR 2022/3, decides everything that follows.

On the same $198,000 of revenue, the difference between the two outcomes is real money — not because one is “cheating” and the other isn’t, but because they’re structurally different arrangements with different tax consequences by design. If PSI attribution applies, the income is treated essentially as if you were an employee, with no company-structure benefit surviving at all. If you genuinely run a Personal Services Business, the company structure delivers real tax planning flexibility.

How PSB status is determined

You can self-assess as a PSB if you pass the results test for at least 75% of your income — meaning you’re paid to produce a specific result, you supply your own tools, and you’re liable to fix defects at your own cost. Failing that, you need the 80% rule (less than 80% of income from one client) plus one of the unrelated clients, employment, or business premises tests. If 80% or more of your income comes from a single client, the results test is your only path — otherwise you need a formal determination from the ATO.

This is a genuine judgement call resting on the specific facts of your engagement, not something a calculator can determine for you — see our dedicated article on the four tests for the full detail.

If you’re a genuine PSB: the franking credit mechanism

Where the PSB pathway gets genuinely interesting is dividend imputation. Your company pays 25% tax (assuming it qualifies as a “base rate entity”) on profit after your director’s salary and superannuation. The remaining after-tax profit can be distributed as a franked dividend, and here’s the key mechanism: the shareholder declares the grossed-up dividend — cash received plus the tax the company already paid — then claims that company tax as an offset against their personal tax bill. Since 2000, excess franking credits are fully refundable, meaning if your marginal rate sits below 25%, you can genuinely receive a cash refund.

If PSI attribution applies: no structuring benefit at all

If the PSI rules apply, the company structure delivers nothing — income is attributed straight to you personally, deductions are limited to what an employee could claim for the same work (no family wages, no home office beyond what an employee could claim, no second vehicle), and there’s no company tax, no dividend, no franking credit to speak of. It’s taxed essentially like a very high-paying job.

A worked comparison

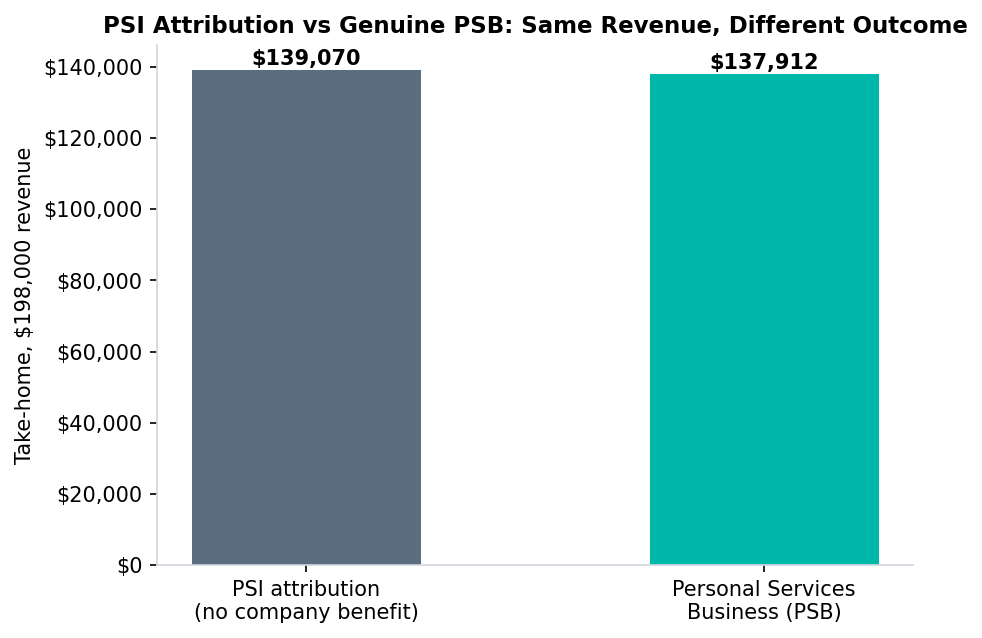

On $900/day × 220 days ($198,000 revenue), with an $18,200 director’s salary under the PSB pathway: company tax is $44,404, the franking credit is $44,404, and take-home lands at $137,912. Under PSI attribution on the same revenue: no company structure at all, tax of $54,970, Medicare Levy of $3,960, take-home of $139,070. Notice the PSI figure is actually slightly higher here — because the PSB pathway’s $2,184 employer super contribution is real money leaving take-home to go into superannuation, not lost, but genuinely deferred. The comparison depends heavily on your salary choice and full circumstances, which is exactly why this needs individual modelling, not a rule of thumb.

Model both pathways with your own day rate using our free contractor calculator — toggle between PSB and PSI attribution to see the real difference.