Salary sacrificing into super is one of the most commonly recommended tax strategies in Australia — and for good reason, though it isn’t universally the right move for everyone. Here’s the actual mechanics, with real numbers, so you can judge for your own situation rather than taking the general advice on faith.

The basic mechanism

Salary sacrifice means agreeing with your employer to redirect part of your pre-tax salary into your super fund, instead of receiving it as cash. Because it’s deducted before income tax is calculated, it reduces your taxable income — and the sacrificed amount is taxed at a flat 15% inside the super fund, rather than at your marginal income tax rate.

Where the saving actually comes from

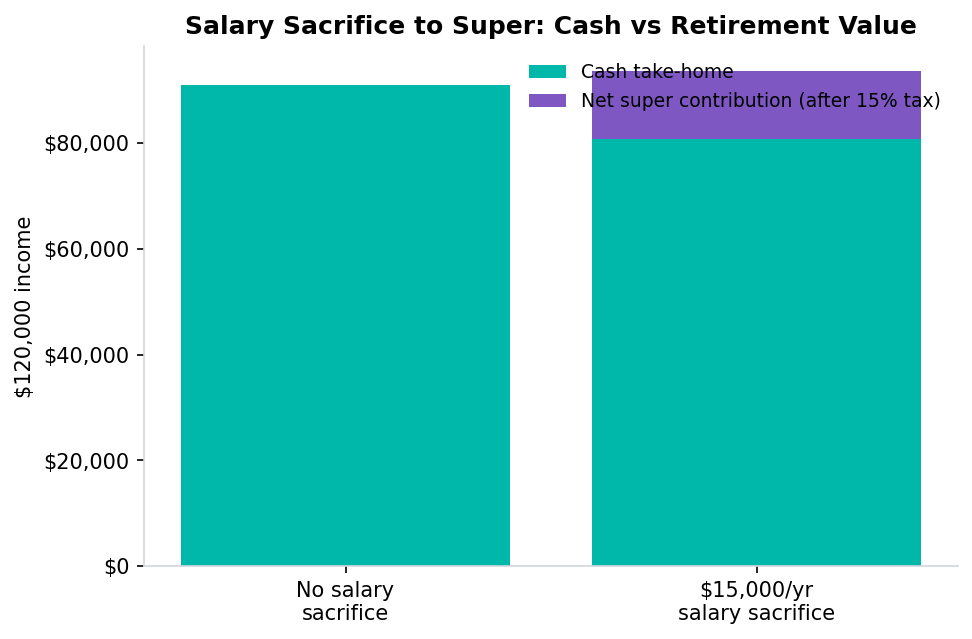

On a $120,000 salary, sacrificing $15,000 a year: without any sacrifice, your marginal rate on that $15,000 would be 30%, meaning roughly $4,500 in tax. Inside super, that same $15,000 is taxed at 15% — $2,250 — leaving $12,750 in your fund rather than roughly $10,500 you’d have kept as cash after standard income tax. The saving is real, but it comes with a genuine trade-off: that money is now locked away in super, generally inaccessible until you meet a condition of release (typically retirement age), rather than available as cash today.

Who this makes the most sense for

The tax saving scales with your marginal rate — it’s most valuable for anyone in the 30% bracket or above, where the gap between your marginal rate and the flat 15% super rate is largest. Below that, particularly if you’re in the tax-free threshold or the 15% resident bracket, the tax benefit shrinks or disappears entirely, since you might be paying close to 15% on that income already.

The concessional cap constrains how much you can do

Salary sacrifice counts toward the same $32,500 concessional contributions cap (2026/27) that also includes your employer’s compulsory 12% Superannuation Guarantee. If your SG contribution is already substantial — which it will be at higher salaries — there may be less headroom for additional salary sacrifice than you’d expect before you’d be contributing beyond the concessional limit and losing the tax benefit on the excess.

What it doesn’t reduce

Salary sacrifice reduces your taxable income for income tax and Medicare Levy purposes — but it does not reduce your HECS-HELP repayment income, since reportable super contributions are specifically added back for that calculation. If you have a HECS-HELP debt, don’t expect salary sacrifice to lower your compulsory repayment; it won’t.

So is it worth it?

This comes down to a genuine personal judgement: how much do you value the tax-efficient growth and forced savings discipline of getting money into super now, versus keeping it accessible as cash for near-term needs — a house deposit, debt repayment, or simply flexibility? Whether salary sacrifice is worth it depends on your age, your other financial priorities, and how comfortable you are locking money away for decades — there’s no universally correct answer for everyone.

Model your own salary sacrifice scenario, including the concessional cap and HECS-HELP interaction, with our free salary calculator.