The Medicare Levy and the Medicare Levy Surcharge are two entirely different things that happen to share a name — and mixing them up is the single most common Medicare-related confusion we see. Here’s the difference, and what each actually costs you.

The Medicare Levy: 2% for most residents

The Medicare Levy funds Australia’s public health system and applies to almost all residents, regardless of whether you use public or private healthcare. For 2026/27 it’s a flat 2% of taxable income — with one important exception for lower incomes.

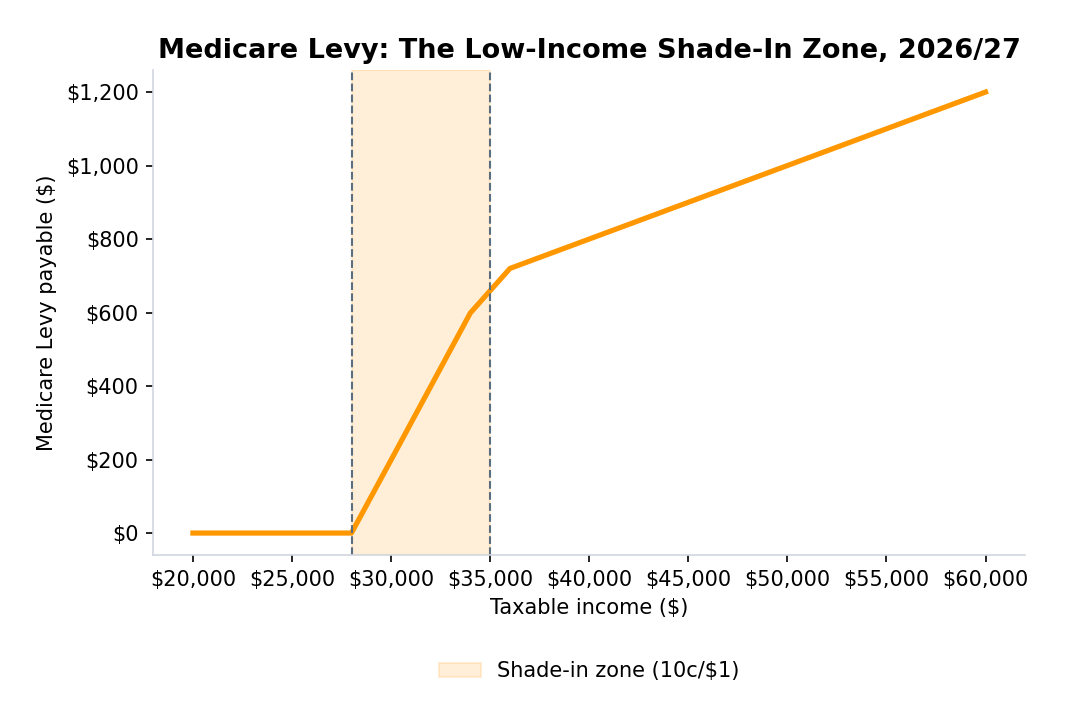

The low-income shade-in zone

If your taxable income is $28,011 or below, you pay no Medicare Levy at all. Between $28,011 and $35,013, the levy phases in at 10 cents for every dollar over $28,011, rather than jumping straight to 2%. Above $35,013, the full 2% applies to your entire taxable income.

On a $30,000 income, for example, you’d pay just $198.90 in Medicare Levy — not the $600 a flat 2% would suggest. This shade-in mechanism exists specifically so the levy doesn’t create a harsh cliff-edge for low-income earners.

Non-residents and working holiday makers are exempt from the Medicare Levy entirely, since they’re not eligible for Medicare benefits in the first place.

The Medicare Levy Surcharge: a different animal

The Medicare Levy Surcharge (MLS) is an additional charge — on top of the 2% levy — that applies only if you don’t hold an appropriate level of private hospital cover and your income is above the threshold. It exists specifically to encourage higher earners to take out private cover rather than relying solely on the public system.

For 2026/27, the surcharge is tiered for singles:

| Income for MLS purposes | Surcharge rate |

|---|---|

| $105,000 or less | 0% |

| $105,001 – $123,000 | 1% |

| $123,001 – $164,000 | 1.25% |

| $164,001+ | 1.5% |

Family thresholds are double the single thresholds, plus $1,500 for each dependent child after the first. The surcharge is calculated on your whole taxable income once you’re over the threshold, not just the amount above it — which is exactly why so many people find that basic hospital cover costs less than the surcharge itself.

Avoiding the surcharge

To avoid the MLS you need appropriate private patient hospital cover — specifically hospital cover, not an extras-only policy — held for the entire income year. Take it out partway through the year and you’ll still owe the surcharge for the days you weren’t covered.

Want to see exactly how much MLS applies to your own income? Our salary calculator includes a “no private hospital cover” toggle that applies the correct tier automatically.