Franking credits are one of the most distinctively Australian features of the tax system — there’s genuinely no direct equivalent in the UK, US, or most other jurisdictions. If you’ve ever seen “franking credit” on a dividend statement and wondered what it actually means for your tax bill, here’s the mechanism laid out plainly.

The problem franking credits solve

Without dividend imputation, company profit would effectively be taxed twice: once as company tax when the company earns it, and again as personal income tax when it’s paid out to shareholders as a dividend. Australia’s imputation system exists specifically to prevent that double taxation.

How franking credits are actually explained in practice

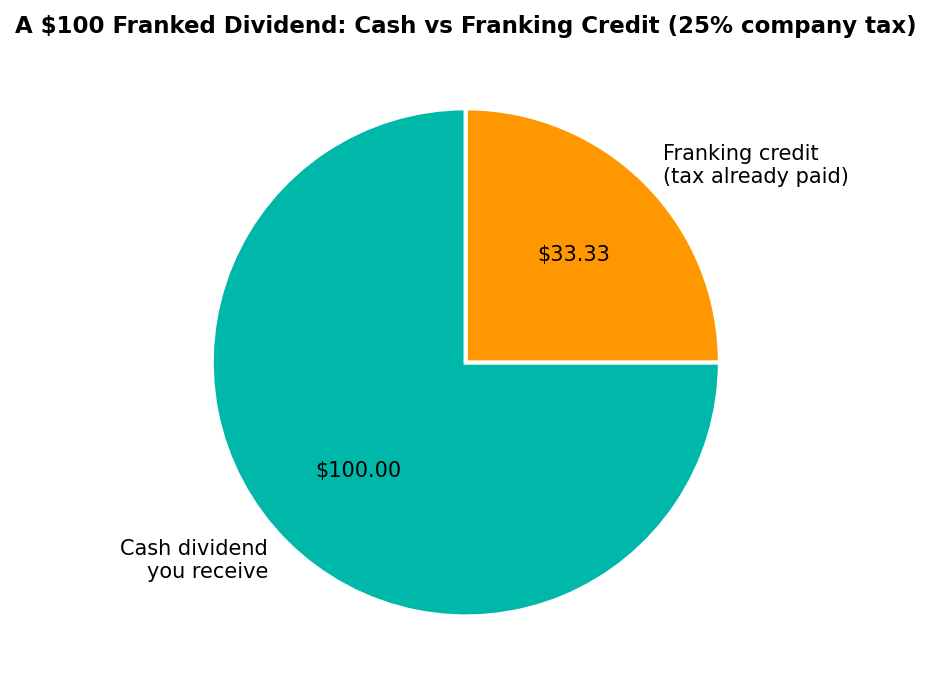

When a company pays tax on its profit, it can attach a “franking credit” to any dividend it distributes, representing the tax already paid. Here’s a $100 fully franked dividend from a company taxed at 25% (the base rate entity rate):

You receive $100 cash, but for tax purposes you declare the grossed-up amount — $133.33 — representing the pre-tax profit the $100 came from. You then get a $33.33 tax offset (the franking credit) against your personal tax bill. If your marginal rate is above 25%, you pay the difference. If it’s below 25%, since 1 July 2000 the excess credit is fully refundable — a genuine cash refund, not just a reduction to zero.

The gross-up formula

The formula the ATO uses: grossed-up dividend = cash dividend ÷ (1 − company tax rate). For a base rate entity at 25%: $100 ÷ 0.75 = $133.33, giving a franking credit of $33.33. For a standard 30% company: $100 ÷ 0.70 = $142.86, giving a larger franking credit of $42.86 — the higher the company’s tax rate, the bigger the credit, because more tax was paid on that profit before it reached you.

Why this matters for contractors

If you contract through a Pty Ltd company and genuinely qualify as a Personal Services Business, franking credits are the mechanism that makes the company structure worthwhile rather than merely an administrative detour. Retained profit is taxed once at the company rate; distributed profit is effectively taxed once at your personal marginal rate, with the franking credit preventing any double-count. It’s genuinely tax-neutral in aggregate — the benefit comes from timing and from any gap between your marginal rate and the company rate, not from avoiding tax altogether.

Partly franked and unfranked dividends

Not every dividend carries the maximum franking credit. A company might distribute a partly franked or entirely unfranked dividend — typically because it hasn’t paid enough Australian company tax to fully frank the distribution (common for companies with significant offshore income, for instance). An unfranked dividend is simply ordinary assessable income with no offset attached.

The 45-day holding rule

To claim franking credits, shares generally need to be held “at risk” for at least 45 days (90 for certain preference shares) — a rule specifically aimed at preventing people from buying shares just before a dividend date purely to capture the credit. This rule doesn’t apply to smaller shareholders whose total franking credits for the year are under $5,000, which covers most individual contractors running their own Pty Ltd.

See the franking credit mechanism applied to your own contracting income with our Pty Ltd contractor calculator.