Not every Australian company pays the same rate of tax — and for most small contractor Pty Ltd companies, that’s genuinely good news. Here’s what a “base rate entity” is, and why the distinction is worth understanding rather than just assuming.

Two company tax rates

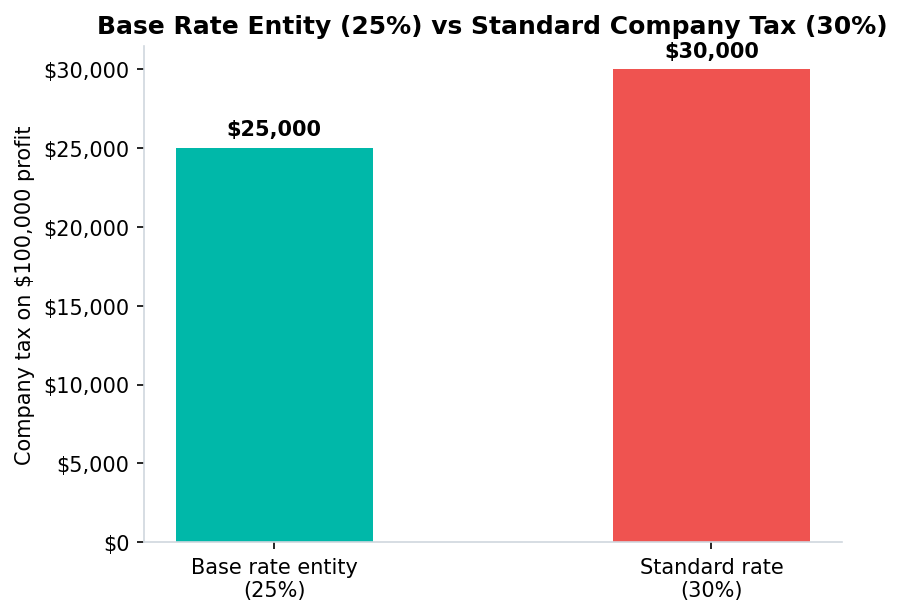

Australia’s standard company tax rate is 30%. But companies that qualify as “base rate entities” pay a reduced rate of 25% — a difference that compounds meaningfully over time, and directly affects the size of franking credits your company can pass on to you.

On $100,000 of company profit, that’s the difference between $25,000 and $30,000 in company tax — $5,000 that either stays in the business or, eventually, reaches you as a larger franked dividend.

What makes a company a “base rate entity”

Two conditions, both need to be met:

- Aggregated turnover under $50 million for the income year

- No more than 80% of assessable income is “base rate entity passive income” (BREPI)

For most small contractor Pty Ltd companies — a single director providing genuine services to clients — both conditions are met easily. The turnover threshold is far above what an individual contractor typically bills, and active service income isn’t passive income at all.

What counts as passive income (BREPI)

Passive income includes things like dividends from other companies (unless you hold a significant voting interest), interest, rent, royalties, and net capital gains. If your Pty Ltd is genuinely trading — billing clients for your services — essentially none of your income falls into this category, so the 80% test is comfortably passed. This provision exists mainly to stop passive investment vehicles from claiming the concessional trading-business rate, not to catch ordinary contractors.

Why this matters for franking

The rate your company actually paid determines the maximum franking credit you can attach to a dividend — you can’t frank at 30% if you only paid 25% tax. For imputation purposes, you assume your turnover and passive income mix will be the same as the previous year, which is how you determine the correct franking rate to apply before you know the current year’s final figures with certainty.

Don’t assume — check

The distinction matters enough that getting it wrong has real consequences: franking a dividend at the wrong rate means either over-franking (which can trigger additional tax) or under-franking (leaving value on the table for your shareholders). For the overwhelming majority of solo contractor Pty Ltd companies, 25% is the correct rate — but it’s worth confirming with your accountant rather than assuming, particularly in a year with unusual passive income (a large asset sale, for instance) that could tip the 80% test the wrong way.

Our contractor calculator assumes base rate entity status (25%) by default, matching the overwhelming majority of solo contractor Pty Ltd companies — but do verify this applies to your specific circumstances.