If you have a HECS-HELP debt, understanding exactly when repayments kick in — and how they’re calculated — matters more than most people realise. This guide gets HECS-HELP repayments explained properly, because the system changed to a genuinely different structure recently, and a lot of the “common knowledge” about how it works is now out of date.

The marginal repayment system

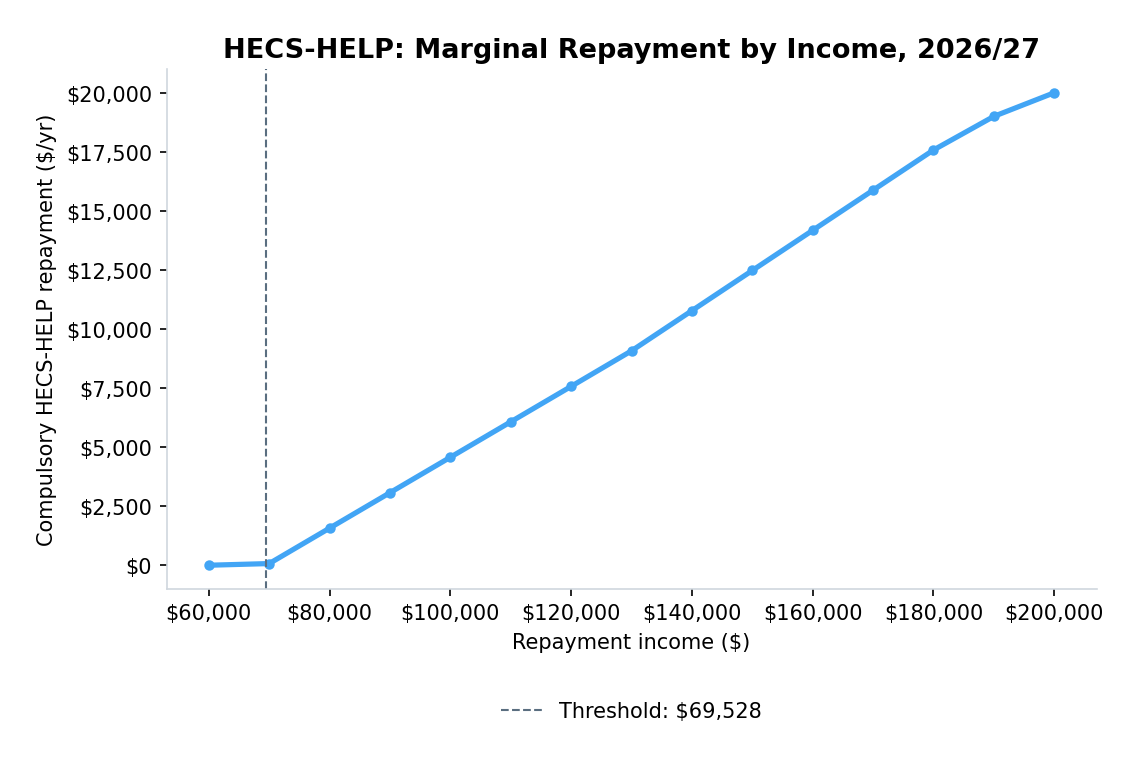

HECS-HELP now uses a marginal repayment system, similar in spirit to how income tax brackets work — you only repay at the higher rate on the portion of income above each threshold, rather than a single rate applying to your entire income the moment you cross a line.

For 2026/27, the bands are:

| Repayment income | Rate |

|---|---|

| Up to $69,528 | Nil |

| $69,528 – $129,717 | 15% of the excess over $69,528 |

| $129,717 – $186,050 | $9,028 plus 17% of the excess over $129,717 |

| $186,050+ | 10% of your total repayment income |

On a repayment income of $100,000, for instance, the repayment is 15% of the amount over $69,528 — ($100,000 − $69,528) × 15% = $4,570.80. This is a meaningfully smaller repayment than the old flat-percentage system would have produced at the same income, and is one of the more genuinely helpful recent reforms to the scheme.

“Repayment income” isn’t just your salary

This is the detail that catches people out: repayment income isn’t simply your taxable salary. It also includes any reportable fringe benefits, net investment losses, and — importantly — any reportable super contributions, including salary sacrifice. If you’re salary sacrificing into super specifically to reduce your taxable income, be aware that HECS-HELP repayment income adds that sacrificed amount straight back in — the strategy reduces your income tax, but not your HECS repayment.

It’s compulsory, deducted through your pay

If your income is above the threshold, your employer is required to withhold additional PAYG specifically for your HECS-HELP repayment, based on the tax file number declaration where you indicate you have a study loan. This isn’t optional once you’re above the threshold — it happens automatically through the payroll system, the same way income tax withholding does.

Voluntary repayments

You can also make voluntary repayments on top of the compulsory amount to pay down the debt faster. Whether this is worthwhile depends on your specific financial position — HECS-HELP debt doesn’t carry interest in the traditional sense (it’s indexed to inflation rather than charged a market interest rate), which is a materially different proposition from most other forms of debt, and changes the calculus on whether early repayment is actually the best use of your money.

See exactly how HECS-HELP affects your take-home pay at your own income with our free salary calculator.