If you contract through a company or trust, working out whether the Personal Services Income rules apply to you comes down to a specific set of tests — and getting this determination right matters, because it decides whether your company structure delivers any real benefit at all.

Start here: the 80% rule

Before you look at any of the other tests, check whether 80% or more of your income in the year comes from one client (including that client’s associates). If it does, your only path to Personal Services Business status is the results test below — you can’t rely on any of the other three tests, and if you don’t pass the results test either, you’ll need a formal PSB determination directly from the ATO rather than being able to self-assess.

Test 1: The results test

The most direct path to PSB status. You need to meet all three conditions for at least 75% of your PSI:

- You’re paid to produce a specific result, not simply for hours worked

- You’re required to supply your own equipment and tools (where the work requires them)

- You’re liable to fix any defects in your work at your own cost, rather than being paid regardless

This test is available regardless of whether you pass the 80% rule — it’s the one universal path.

Test 2: The unrelated clients test

You need PSI from two or more clients who aren’t associated with each other or with you, gained as a direct result of making offers to the public at large — a genuine website, advertising, tendering for work, or word-of-mouth referrals from that public-facing presence. Work obtained through a labour hire arrangement doesn’t qualify under this test.

Test 3: The employment test

Your business needs to employ or contract others to perform at least 20% of the principal work that generates your PSI — or employ one or more apprentices for at least six months of the year. This is the test that most clearly signals “this is a business with staff,” rather than one person’s labour running through a company.

Test 4: The business premises test

You maintain and use business premises — physically separate from your home and from your client’s premises — that you have exclusive use of for the purpose of your business, for the whole of the relevant period.

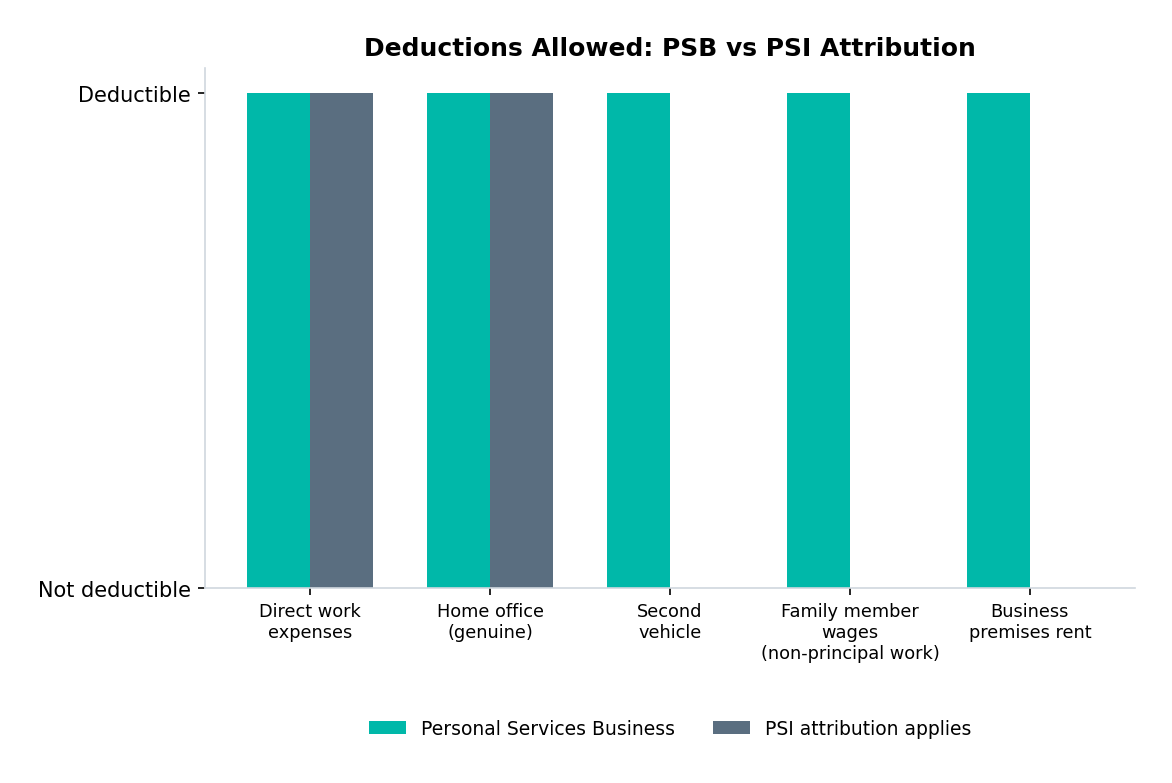

What’s actually at stake: deductions

The practical consequence of the determination is deductions. A genuine PSB retains the full range of ordinary business deductions. Under PSI attribution, you’re limited to roughly what an employee doing the same work could claim — direct work expenses and a genuine home office are still available, but a second vehicle, wages paid to family members for non-principal work, and business premises rent generally aren’t.

This is a judgement call, not a checklist

The ATO’s own guidance (TR 2022/3 and, more recently, PCG 2025/5) makes clear this rests on the specific facts of your engagements, applied individually if more than one person in your business generates PSI — it’s genuinely possible for one person to run a PSB while another, in the same company, is subject to PSI attribution. If your situation isn’t clear-cut, this is worth a conversation with a registered tax agent before you rely on a self-assessment.

Once you’ve made your own determination, our contractor calculator lets you model the actual tax outcome under whichever pathway applies to you.