Here’s a fact that surprises a lot of new sole traders in Australia: unlike an employee, nobody is legally required to pay superannuation on your behalf. If you don’t do it yourself, it simply doesn’t happen — there’s no employer sitting behind you making the 12% contribution automatically.

Why the Superannuation Guarantee doesn’t apply to you

The Superannuation Guarantee (Administration) Act 1992 obliges employers to contribute 12% of an employee’s ordinary time earnings to super. As a sole trader, you are, legally, not your own employee — there’s no employer relationship for the Act to attach to. This isn’t an oversight or a loophole; it’s simply outside the scope of what the SG scheme was built to cover.

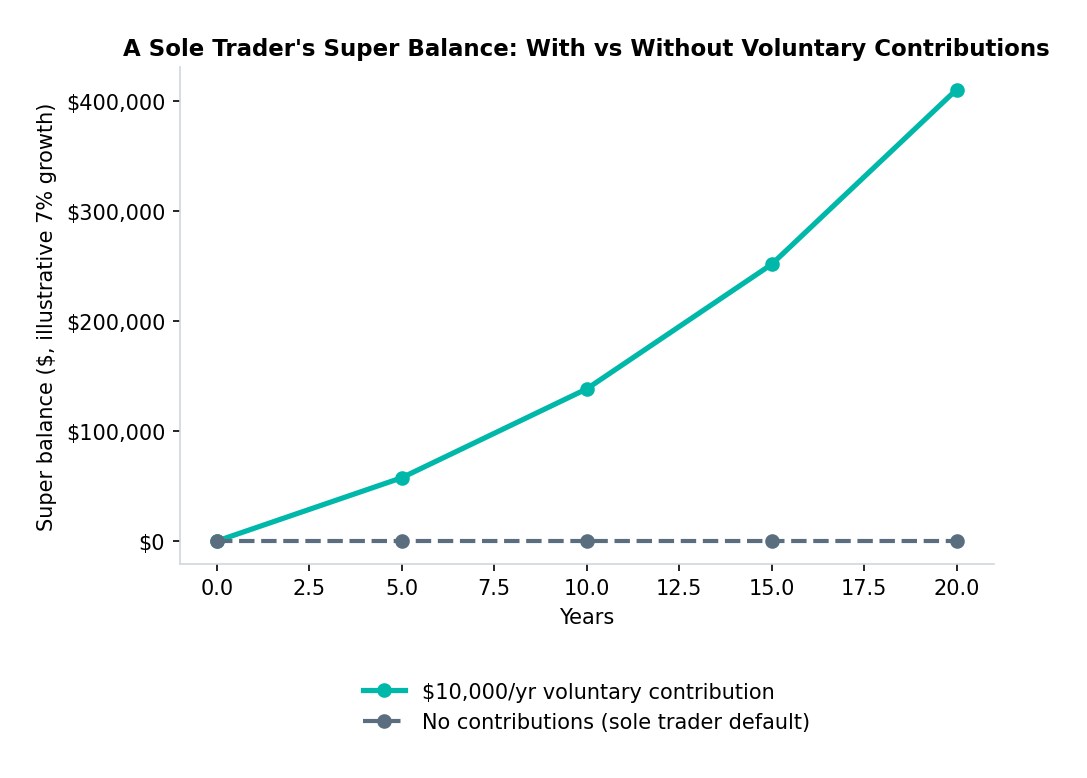

The compounding cost of doing nothing

The gap this creates compounds over time in a way that’s easy to underestimate. Contributing $10,000 a year at an illustrative 7% growth rate builds to a genuinely substantial balance over 20 years — while doing nothing leaves you with exactly nothing from this source, relying entirely on the Age Pension and whatever personal savings you’ve built outside super. This isn’t a scare tactic; it’s simply the mechanical reality of compound growth applied over decades, which is precisely the timeframe super is designed around.

Personal deductible contributions

The standard tool for closing this gap is a personal deductible contribution — you contribute directly to your own super fund and claim a tax deduction, exactly as an employee’s salary sacrifice reduces their taxable income. The contribution is taxed at a flat 15% inside the fund, rather than at your marginal tax rate, which is a genuine saving for anyone in the 30% bracket or above, quite separate from the retirement benefit itself.

The concessional contributions cap for 2026/27 — the annual limit on contributions taxed at the concessional 15% rate — is $32,500. Contribute beyond that and the excess is taxed at your marginal rate instead, losing the concessional benefit.

The government co-contribution

If you’re a low or middle income earner making personal (non-deductible) contributions, the government may add its own co-contribution on top — worth checking if your income sits in the eligible band, since it’s effectively a guaranteed top-up on your own savings.

What most sole traders actually do

In practice, many sole traders treat super as something to fund from profit at tax time, once they know their actual annual result, rather than a fixed monthly commitment the way PAYE withholding forces on employees. There’s no wrong answer here as long as it’s a deliberate decision rather than something that simply never happens because there’s no automatic mechanism forcing it.

Our sole trader calculator lets you model a personal deductible super contribution against your actual profit, so you can see the real tax saving before deciding how much to set aside.